How Can Credit Scores Impact Home Loans?

Did you know that two identical mortgage applications can yield vastly different outcomes due solely to a three-digit number? The credit score acts as a numeric shorthand for a borrower’s reliability in repaying debts. This can dramatically affect the interest rates offered and the size of the loan approved, essentially being the key that unlocks or closes the door to homeownership.

Historically, credit scores have existed as a gatekeeper in the lending process since the 1980s. Mortgage lenders lean heavily on scores to determine risk levels; an astonishing 90% of top lenders use FICO scores. Consequently, bolstering one’s credit score can potentially save thousands of dollars over the life of a mortgage, making it a significant element of financial planning for prospective homeowners.

The Role of Credit Scores in Home Loans

Credit scores play a crucial part in deciding who gets a home loan. Lenders consider these scores as an indicator of your financial health. A high score often signals you’re good at managing debt. This can lead to better loan offers with lower interest rates. On the flip side, a low credit score might limit your options.

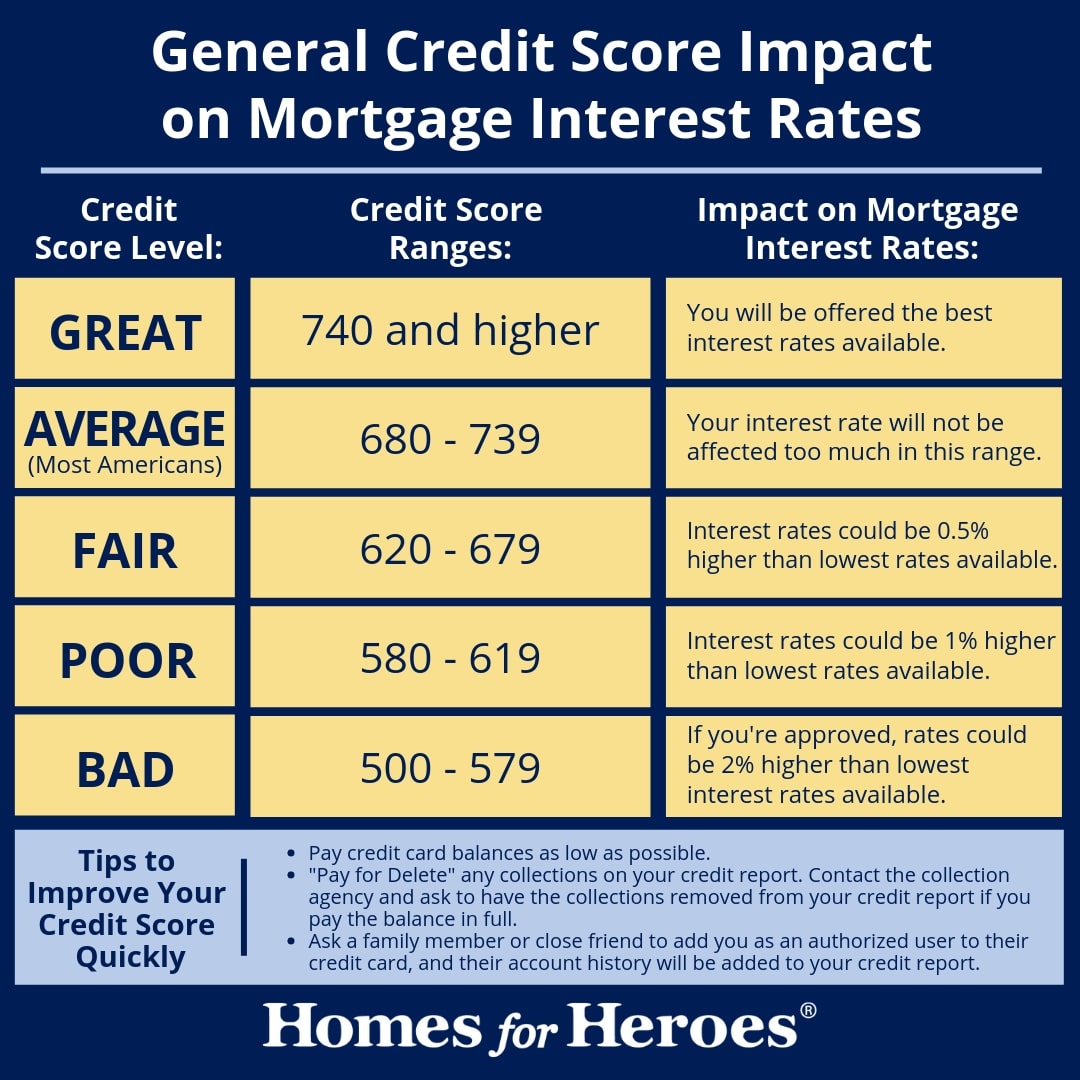

Lenders aim to minimize risk, so they rely on credit scores heavily. They want to make sure you’ll be able to pay back the loan. Scores usually range from 300 to 850, with higher scores being better. Each lender may have its own minimum score requirement. It’s important to understand how these numbers affect your mortgage chances.

A poor credit score can result in higher interest rates. This means you’ll pay more over time. For instance, owing an extra 1% interest could add thousands to your loan cost. Some lenders might not even offer a loan if the score is too low. This makes improving your score a big priority for many.

To boost your credit score, handle bills promptly and avoid large debts. Other actions include checking your credit report for mistakes. You may also consider getting professional help. It can take a while to see changes, but it’s worth it. With a better score, you’ll have more beneficial loan options.

Importance of FICO scores in Home Loan Approval

FICO scores hold significant weight when getting approved for a home loan. Lenders use these scores to determine the likelihood of a borrower repaying the loan. A high FICO score suggests that a person has consistently paid their debts on time. This provides lenders with confidence in the borrower’s financial responsibility. As a result, they may offer better loan terms.

A list of key factors influencing FICO scores includes:

- Payment history

- Debt amounts

- Length of credit history

- New credit inquiries

- Types of credit used

Each of these factors impacts the score differently. Borrowers should focus on strengthening these areas to improve their FICO score.

A lender often sets a minimum FICO score requirement for loan approval. Failing to meet this threshold can mean missing out on a loan altogether. Even a few points can make the difference between approval and denial. Thus, understanding and improving one’s FICO score is crucial. Consistent monitoring of your credit status is also advisable.

Borrowers with higher FICO scores stand to benefit from lower interest rates. These rates significantly impact monthly mortgage payments. For example, a small difference in interest rates can lead to thousands in savings over the loan’s life. This makes maintaining a good FICO score beneficial. Borrowing becomes less costly, ensuring financial peace of mind.

Impact of Low Credit Scores on Home Loans

Low credit scores can create hurdles when applying for a home loan. Lenders see these scores as a sign of risk, which can affect the type of loans available. Borrowers with lower scores might only qualify for loans that have less favorable terms. These terms often include higher interest rates that make monthly payments more expensive. This can increase the overall cost of owning a home significantly.

Some challenges faced by borrowers with low credit scores include:

- Fewer loan options available

- Increased down payment requirements

- Additional fees or insurance premiums

- More stringent approval processes

These obstacles make it more difficult to secure a loan. However, recognizing these challenges can guide borrowers to improve their credit scores.

Additionally, a low credit score may require a cosigner for loan approval. This involves having someone with a better score vouch for the borrower. Lenders might feel more comfortable providing a home loan under these conditions. Although this can be a solution, finding the right cosigner is crucial. A strong collaboration can help overcome score-related barriers.

Improving a low credit score takes time and effort but pays off in the long run. Steps such as paying bills on time and reducing outstanding debts can help increase scores. Access to better loan terms becomes a real possibility with these improvements. It’s also beneficial to regularly monitor the credit report for errors. Identifying and correcting these errors can further boost credit health.

Advantages of High Credit Scores for Mortgage Borrowers

High credit scores present many benefits for mortgage borrowers. Lenders see these scores as an assurance of the borrower’s ability to repay loans. Consequently, they often offer better loan terms. A key advantage is lower interest rates, which translate into reduced monthly payments. This means substantial savings over the term of the mortgage.

Borrowers with excellent credit scores may access a wider range of loan options. This choice allows borrowers to select what best fits their needs and goals. For instance, more flexible loan terms might be available. Lenders might offer a variety of repayment plans. Such flexibility can lead to a more affordable and manageable mortgage.

Another benefit of a high credit score is the possibility of a smaller down payment. Some lenders may require less money upfront from borrowers they trust. This can significantly ease the financial burden during the home-buying process. Lower initial payments can also free up funds for other expenses. This makes it easier for buyers to manage their finances.

Borrowers with strong credit scores may also avoid private mortgage insurance (PMI). PMI is often required when a down payment is below 20%. However, lenders may waive this requirement for trusted borrowers. Avoiding PMI can further lower monthly costs. This means even more savings for the homeowner over time.

Additionally, the approval process tends to be smoother for those with high credit scores. Lenders have confidence in the borrower’s financial history and reliability. As a result, they often handle applications more quickly and with less red tape. This can make the home-buying journey less stressful. Faster approvals can help in competitive markets where timing is crucial.

Strategies to Improve Credit Scores for Better Home Loan Terms

Boosting your credit score can open doors to better home loan terms. One effective strategy is to consistently pay bills on time. Lenders want to see reliable payment history over time. Setting up automatic payments or reminders can help ensure bills are paid promptly. This simple action can gradually improve your credit score.

Reducing outstanding debt is another key move. Lenders look at how much debt you carry in relation to your credit limit. Aim to keep your credit utilization ratio below 30%. Paying down existing balances is a step in the right direction. This signals to lenders that you’re managing your debt well.

Regularly checking your credit report for errors is crucial. Sometimes mistakes can lower your score unfairly. Scrutinize your report for inaccuracies and dispute them promptly. Correcting these mistakes can lead to an immediate boost in your score. It’s wise to review your report annually to stay informed.

Another helpful tactic is to avoid opening too many new accounts at once. Each application for credit can slightly lower your score. Lenders may see multiple applications as a sign of financial trouble. Instead, focus on gradually building credit over time. Being mindful of the accounts you open can maintain a healthier credit profile.

Lastly, consider becoming an authorized user on a trusted person’s credit card. This allows you to benefit from their positive payment history. Ensure the primary account holder is responsible with payments. This can lead to credit score improvements over time. Sharing credit can be an effective way to boost your score responsibly.

Credit Scores and Mortgage Rates: An Unavoidable Connection

Credit scores play a big role in determining mortgage rates. Lenders use these scores to judge how likely you are to repay your loan. A high score often leads to lower interest rates, making your mortgage more affordable. Conversely, a low score can mean paying more over time. This direct link influences the overall cost of homeownership.

Mortgage rates can vary greatly based on credit scores. For instance, someone with excellent credit might receive a rate of 3%, while a lower score could raise the rate to 4% or higher. Even a 1% difference can mean thousands of dollars over a 30-year loan. This makes it crucial to know your credit status. By improving your score, you could save a lot in the long run.

A list of benefits from maintaining a high credit score includes:

- Access to competitive mortgage rates

- Reduced monthly payments

- Lower overall loan costs

- Improved negotiating power with lenders

Each of these benefits emphasizes the importance of credit scores. They can create real financial advantages when buying a home.

Borrowers with higher scores also have more loan choices. Lenders are more willing to approve mortgages for those with proven financial reliability. This flexibility allows buyers to select loans with terms that suit them best. Having options can make the home-buying process less stressful. Making the right financial choices becomes easier.

Monitoring your credit score regularly is wise. Knowing your score helps you understand what mortgage rates you might face. If your score isn’t where you want it to be, take steps to improve it. Practices like timely payments and debt reduction can lead to score growth. With a better score, you can achieve the best mortgage rates available.

Frequently Asked Questions

Credit scores are a critical aspect when considering home loans. Understanding how these scores influence borrowing can ease the loan process. Here are some common questions to further clarify this topic.

1. What is considered a good credit score for home loans?

A good credit score for home loans generally starts at around 670. Scores above this range can position borrowers for more favorable loan terms. Higher scores often lead to better interest rates and more borrowing options. Lenders prefer these numbers because they indicate a responsible borrower.

However, different lenders might have varying standards for what they deem a good score. Some might offer competitive rates even to those in the mid-600s. Therefore, it’s important to check with different lenders to find the best options. Comparing offers can reveal the advantages of holding a higher score.

2. Why do lenders rely on credit scores when offering loans?

Lenders use credit scores to assess the risk involved in lending money. Scores summarize a borrower’s credit history and financial habits. Credit scores thus help lenders determine how likely a borrower is to repay a loan. This insight is crucial for lenders to make informed decisions.

A good score usually means you’re seen as reliable and low-risk. This reliability translates into trust from lenders, often resulting in better loan terms. Without scores, lenders would need other, less efficient ways to evaluate borrowers. Overall, credit scores simplify and streamline the approval process.

3. Can a high credit score lower monthly mortgage payments?

Yes, a high credit score can lead to lower monthly mortgage payments. This happens because lenders often offer lower interest rates to borrowers with excellent credit. Since the interest rate is a significant part of your mortgage cost, lower rates reduce your monthly expense. This makes managing a loan more affordable over time.

Achieving a high score means lenders deem you financially responsible. As a result, you’re more likely to secure better terms than others. Paying less interest over the loan’s life can also lead to significant savings. A higher score thus simplifies financial planning for homeowners.

4. How often should you check your credit score?

Checking your credit score regularly is a wise practice, recommended every few months. Frequent checks help you spot inaccuracies that could affect your score. Many services provide free credit reports annually, but you can access your score more often. Monitoring your score helps you understand your financial position.

Regular checks ensure you’re not caught off guard by sudden drops. Awareness lets you address any issues quickly, such as unauthorized card usage. By staying on top of your credit score, you can maintain or improve it over time. This vigilance can be incredibly beneficial when planning to apply for loans.

5. How long does it take to improve a credit score?

Improving a credit score can take time and usually requires several months of dedicated effort. Consistently paying bills on time and reducing debt are effective strategies. It’s essential to have patience, as quick fixes rarely lead to sustained improvements. Focus on good habits, and you’ll eventually see positive changes.

The timeline for improvement depends on several factors, like current score and financial history. Some might see progress faster than others. However, making small but consistent changes can have lasting effects. Over the long run, these improvements can lead to better loan terms and financial health.

Conclusion

Understanding the impact of credit scores on home loans is crucial for potential homeowners. A high credit score not only unlocks favorable loan terms but also eases the borrowing process significantly. Proactive steps to maintain or improve one’s credit health can transform the financial landscape. This ensures a sound and strategic approach to homeownership.

As credit scores shape mortgage options and rates, staying informed becomes imperative. Regular monitoring and effective management pave the way for long-term financial savings. By prioritizing financial stability through credit awareness, borrowers position themselves for success. This comprehensive understanding ultimately contributes to a more secure and manageable homeownership journey.